Tesla’s upcoming earnings report highlights the intense competition in the electric vehicle market. As profits decline and pressures mount, investors are anxious for insights into Tesla’s future growth and strategy.

Tesla Earnings to Highlight Competition Challenges

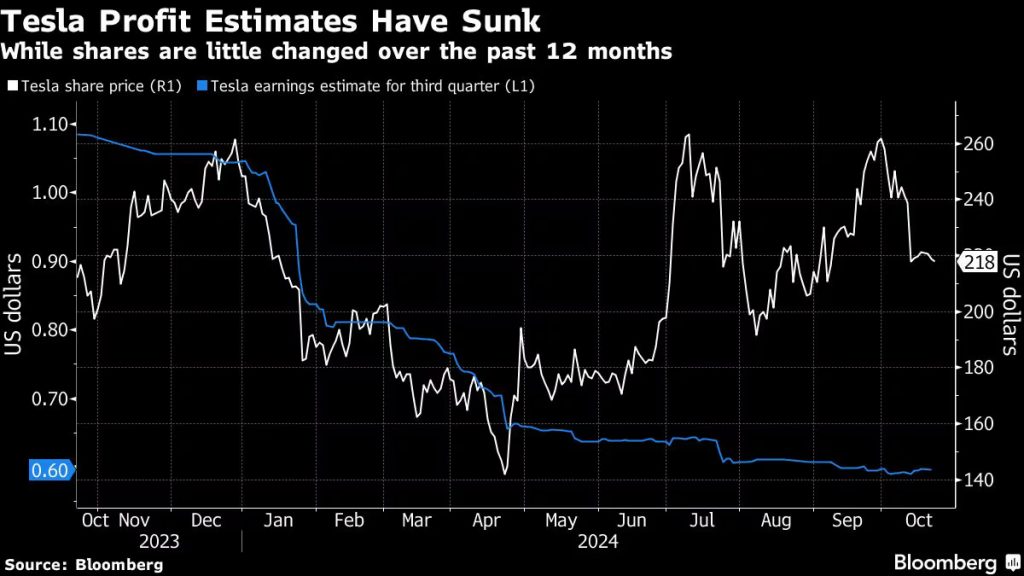

With shares falling and profits shrinking, Tesla Inc. increasingly looks like the odd one out among its mega-cap technology peers. Investors worry that quarterly results will make the electric-vehicle maker even more of an outlier.

Growing Competition in the EV Market

The Elon Musk-led company is the only member of the so-called Magnificent Seven expected to see profits decline in its latest quarterly results — and the only one that has seen Wall Street estimates come down from a year ago. The shares have fallen 12% this year, while all of its Big Tech peers have advanced. Despite that, it remains the most expensive stock in the group when plotted next to profits, creating a challenging setup for earnings.

The results, due on Wednesday after the close, may not have mattered so much if Tesla had impressed investors with its recent reveal of a self-driving car. However, the robotaxi failed to meet high expectations, adding pressure to the company’s core business of selling EVs.

“Investors are starting to lose patience with Tesla, especially after the robotaxi event that was long on idea but short on execution, as growth expectations from their core business remain low over the next two years,” said David Wagner, portfolio manager at Aptus Capital Advisors.

Impact of Competition on Tesla’s Performance

Wall Street will be watching for signs that slowing EV sales are close to a trough while keeping an eye on margins, which have faced pressure over the past year. Investors are also anxious to hear more about a cheaper EV model.

A better-than-expected set of numbers would help restore some confidence in the near term. However, analysts warned that a significant rise for the shares may be difficult without more clarity about long-term growth.

“Regardless of the third-quarter result, we think a sustainably bullish re-rating may not occur until investors have reasons to boost estimates,” Piper Sandler analyst Alexander Potter wrote in a note. Potter expects these reasons to emerge next year, including the unveiling of a new product and regulatory approval for the company’s advanced driver assistance software in a new region, such as China.

Analysts on average expect the company to report earnings per share of 60 cents for the three months ended Sept. 30, representing a 10% decline from the year-ago period. Revenue is estimated to be about $25.4 billion, up 8.9% from the previous year, according to data compiled by Bloomberg.

Monitoring Competition Trends in the EV Market

The third-quarter estimates represent a significant drop from a year ago, when analysts had forecast EPS of $1.09. Meanwhile, the main metric that traders watch — automotive gross margin excluding regulatory credits — is expected to be 14.9%, up slightly from the second-quarter figure of 14.6%.

“The most important factor for the stock in the short term is if demand trends come in above or below expectations and if gross margins are above or below,” said Cole Wilcox, portfolio manager at Longboard Asset Management. While Tesla’s position in the EV market remains strong compared to rivals, “EV demand is not the explosive high-growth category it once was,” Wilcox noted.

Tesla has been at the forefront of a slowdown in EV demand since late 2023, as consumers squeezed by inflation, high borrowing costs, and nervousness about an economic slowdown held off on big-ticket purchases. The company responded by aggressively lowering prices to attract buyers and undercut emerging competition. While this strategy helped win some customers, it hasn’t fully offset weak demand, leading to declines in both revenue and profit.

Tesla’s Valuation Amid Increased Competition

Lower profit expectations have also made Tesla’s stock valuation appear even more pricey. At 74 times forward earnings, it’s the most expensive of the mega-cap group, which includes Amazon.com Inc., Microsoft Corp., Apple Inc., Alphabet Inc., Meta Platforms Inc., and Nvidia Corp.

Still, investors argue that the company’s position among the Magnificent Seven remains valid, given Tesla’s ability to innovate and potentially dominate the auto industry in a future where self-driving vehicles are standard.

“Tesla’s upcoming earnings are crucial, but they’re part of a larger picture,” said Adam Sarhan, founder and chief executive officer at 50 Park Investments. “For now, it’s too early to dismiss Tesla from the Mag 7, but the pressure is certainly on for the company to prove its worth.”

Top Tech Stories

Arm Holdings Plc is canceling a license that allowed longtime partner Qualcomm Inc. to use Arm intellectual property to design chips, escalating a legal dispute over vital smartphone technology.

Apple Inc.’s Chief Executive Officer Tim Cook promised to keep investing in China during a meeting with Beijing’s top technology official, underscoring the country’s vital role in the iPhone maker’s global operations.

An investigation of Huawei Technologies Co.’s latest AI offering has unearthed an advanced processor made by Nvidia Corp. manufacturing partner Taiwan Semiconductor Manufacturing Co., suggesting that China is still struggling to reliably make its own advanced chips in sufficient quantities.

ASML Holding NV Chief Executive Officer Christophe Fouquet expects pressure will grow from the US to further restrict sales of semiconductor technology to China, the biggest market for the Dutch producer of chipmaking machines.